NEED IMMEDIATE ASSISTANCE? CALL US AT 877-997-9473

UNDERSTANDING

EMV

A MERCHANT'S GUIDE TO THE

LIABILITY SHIFT

EMV is the microchip in specific credit cards that sends transaction data to a credit card processor. EMV stands for Europay, MasterCard, and Visa and is an international standard for authenticating debit and credit card transactions.

What is EMV?

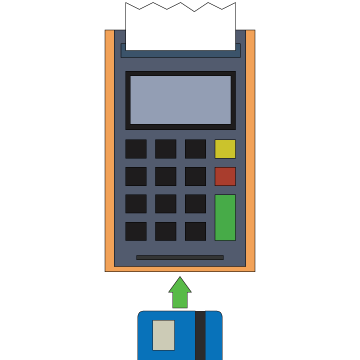

Rather than swiping the payment card, the customer will insert the card face-up, chip-first into the terminal. The card remains in the terminal throughout the entire transaction.

The customer will then sign the receipt or enter their PIN to complete the transaction. The customer may then remove their card from the EMV terminal.

The EMV Transaction Process

EMV's chip-and-PIN and chip-and-signature transactions are considered to be much more secure than the current magnetic stripe technology. Countries that have implemented EMV have seen a dramatic drop in fraud rates.

$103.5B

saved from

card skimming reductions in Canada

Source: http://www.smartcardalliance.org/publications-emv-faq/

67%

reduction in fraud losses in the UK since 2004

1.62B

EMV-enabled payment cards in use throughout

the globe

Why implement EMV?

The Numbers Behind EMV

Liability for fraudulent transactions will fall back on the merchant if the merchant is not using EMV technology.

The Liability Shift

As a merchant, you are responsible for having and properly using an EMV terminal during your transactions. The liability for any fraud or chargeback falls on you, the merchant, if you are not using an EMV terminal.

If a fraudulent retail transaction occurs while you are using an EMV transaction, the liability does not automatically fall on you, but rather the card issuer.

However, if you are running a chip-and-PIN card (as opposed to a chip-and-signature card), and the PIN is bypassed rather than entered, the liability for any transaction automatically falls back on you.

The rule of thumb for liability is that the party using the less-secure technology, whether that be the terminal or the payment card, is typically held liable.

Who's responsible for what?

Upgrading to EMV and becoming prepared for the liability shift does not have to be an overly expensive or time-consuming process.

EMV Preparedness

How do I know if I have an EMV terminal?

An EMV terminal will have a slot in the front of the terminal in which the customer would input their card. However, not all of the terminals with the front dip slot are EMV ready or compliant with the requirements of the liability shift. The best way to ensure you are prepared for the liability shift is to call us at 877-997-9473.

What is the typical cost of an EMV terminal?

The average cost of an EMV terminal ranges from $200 to $300, not including a PIN pad.

Do I need to purchase a PIN pad?

Not necessarily. Certain terminals with internal PIN pads can be encrypted for a fee.

However, if your business does not present the terminal to the customer or you do not have an internal PIN pad, you will be required to purchase an EMV PIN pad. The EMV PIN pads have a slot in the front where the customer slides the payment card in addition to a number pad.

When will I have to get an EMV terminal?

October 1, 2015 is the deadline for EMV implementation.

I accept credit cards online/over the phone. Do I need to become EMV compliant?

The EMV liability shift does not currently apply to transactions that are processed online or over the phone. However, any card-present transactions must be run through an EMV-enabled terminal.

Is my mobile swiper EMV compliant?

We are currently exploring our options regarding EMV-capable mobile swipers. Please click here to receive any updates regarding EMV processing through a mobile device.

Frequently Asked Questions

The external links below offer a more in-depth look at EMV, the liability shift, and how it affects your business.

Resources

Transforming Payments with EMV

MasterCard's EMV information site

Official Visa site for EMV information

CreditCards.com's EMV FAQ with in-depth answers to commonly-asked questions

Helpful Links

PRODUCTS

CONTACT

208 E. Pennsylvania Blvd

Feasterville, PA 19053

Local: (215) 809-1000

Toll-free: (877) 997-9473

Fax: (215) 701-4989

RESOURCES

Copyright 2015 Advanced Merchant Group, Inc. All rights reserved.